Par Value Of Shares

Par Value And No Par Value Stock Youtube

What Is No Par Value Shares Accountant Skills

Par Value And No Par Value Stock Youtube

Share Capital

Par Value The Nominal Or Face Value Of A Bond Or Stock

How To Figure Out Par Value On Balance Sheet The Motley Fool

Par value for stock.

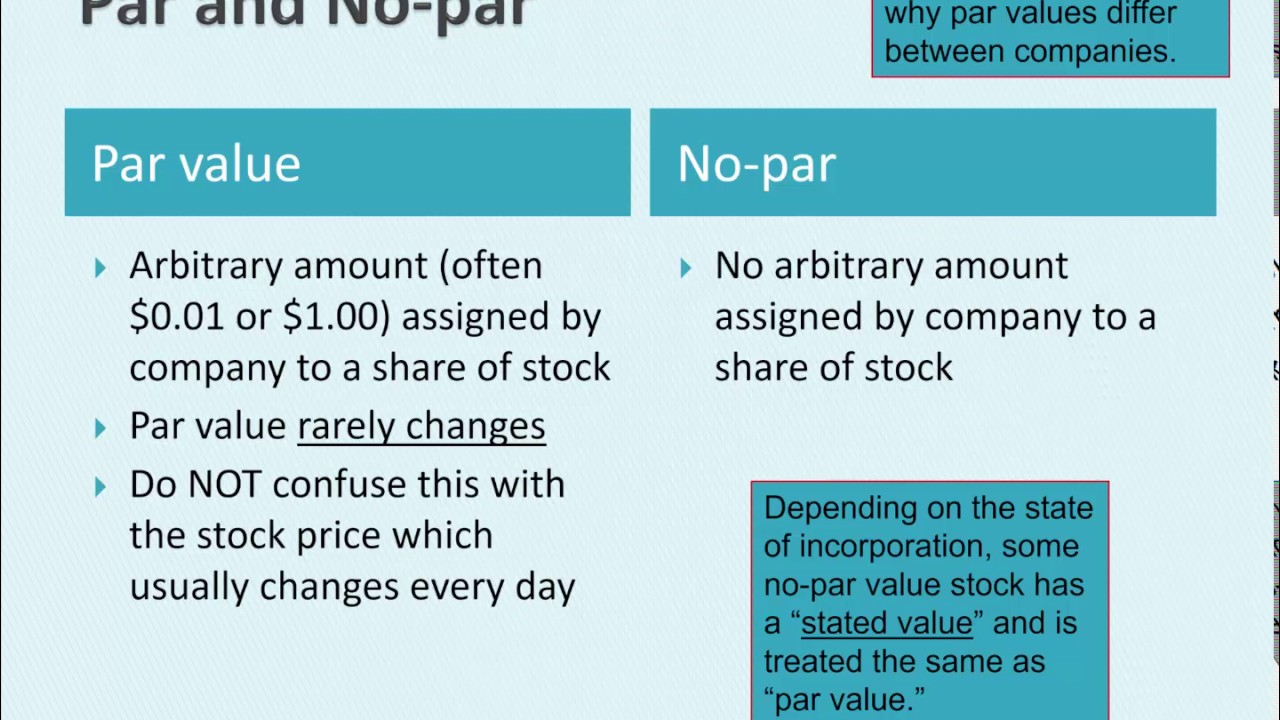

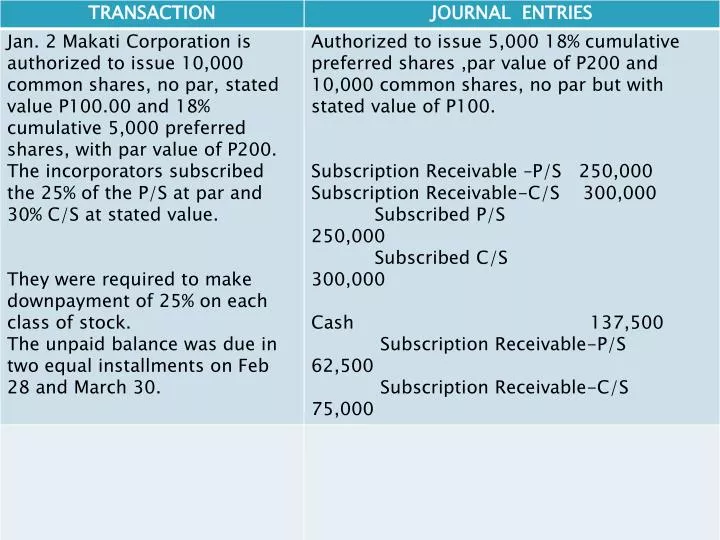

Par value of shares. Par value of shares also known as the stated value per share is the minimal shares value as decided by the company which is issuing such shares to the public and the companies then will not sell such type of shares to the public below the decided value. Par value is important for a bond or fixed income instrument because it determines its maturity value as well as the dollar value of coupon payments. Par value stock. After the implementation date of the companies act a pre existing company may not authorise any new par value shares authorise any shares having a nominal value or do any subdivision thereof.

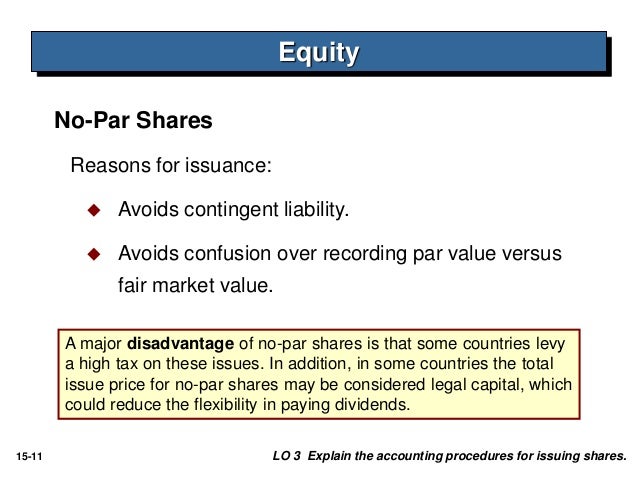

No par value stock is shares that have been issued without a par value listed on the face of the stock certificate historically par value used to be the price at which a company initially sold its shares. There is a theoretical liability by a company to its shareholders if the market price of its stock falls below the par value for the difference between the market price of the stock and the. Par value is likewise important to aspiring entrepreneurs who are starting to form a corporation. The par value of a share is the value stated in the corporate charter below which shares of that class cannot be sold upon initial offering.

The intent behind the par value concept was that prospective investors could be assured that an issuing company would not issue shares at a price below the par value. However par value is now usually set at a minimal amount such as 0 01 per share since some state laws still require that a company cannot. This will be shown as a separate amount in the paid in capital or contributed capital section of. The issuing company promises not to issue further shares below par value so investors can be confident that no one else will receive a more favorable issue price.

When a corporation s common or preferred stock has a par value corporation s balance sheet will report the total par value of the shares issued for each class of stock. For example if a shareholder pays 5 for 1000 shares with a par value of 1 4 000 would be credited to the corporation s paid in capital account and 1 000 to the common stock account. Shares issued in terms of the 2008 act have no nominal or par value. Shares of stock sold at a price above the par value would result in additional paid in capital reflected in the books of the company.

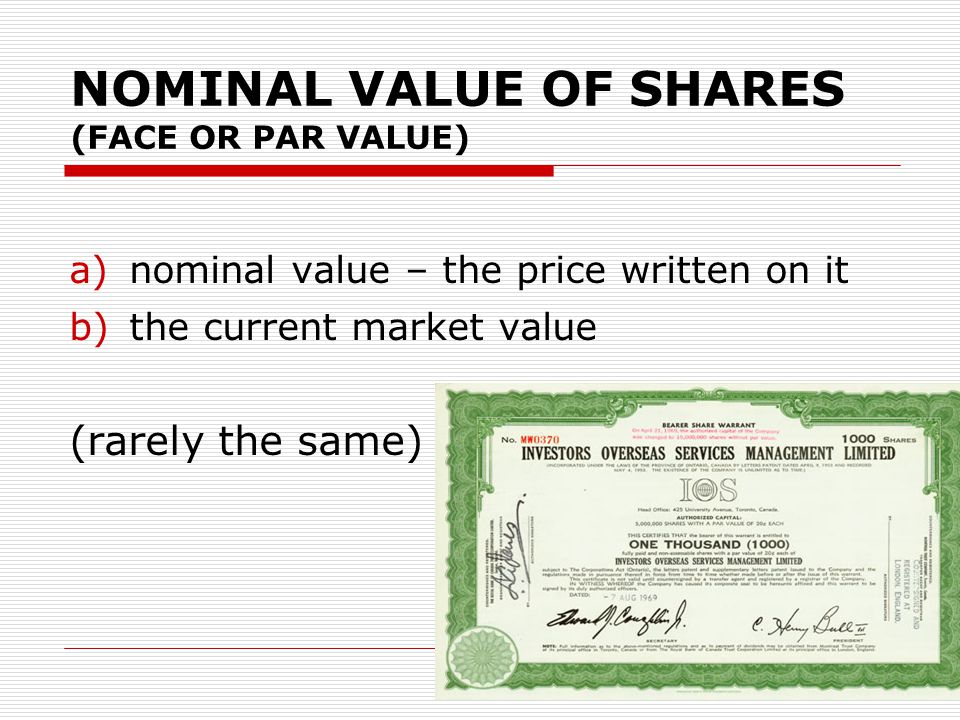

In other words it is the share nominal amount 1 0 1 or 0 001 mentioned on the stock certificate at the time. The capitalization target is readily configured if the company will set a value for each stock offered. The par value is sometimes referred to as the common stock s legal capital. The board must determine the price or other adequate considerations at which shares may be issued.

What is par value of share. Companies sell stock as a means of generating equity capital so the par value multiplied by the total number of shares issued is the minimum amount of capital that will be.

No Par Stock Journal Entry In Accounting Double Entry Bookkeeping

12 1 Capital Stock Transactions

7 Accounting For Equity

Par Value Change In Par Value

Par Value Of Stock Definition Example Effects Youtube

12 1 Capital Stock Transactions

Ppt Legal Capital Aggregate Of The Par Value Of All Issued Par

Par Or No Par Value Shares What Is The Significance

Share Capital

Stocks And Shares Equity Finance Equity Equities Common Stock

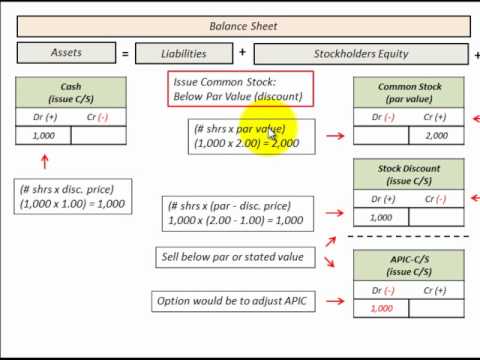

Common Stock Issued With Par Value Vs No Par Value Accounting

How Do I Find The Price Per Share And The Par Value

7 Accounting For Equity